Fintech7 items

Best Banking-as-a-Service (BaaS) Platforms (2026)

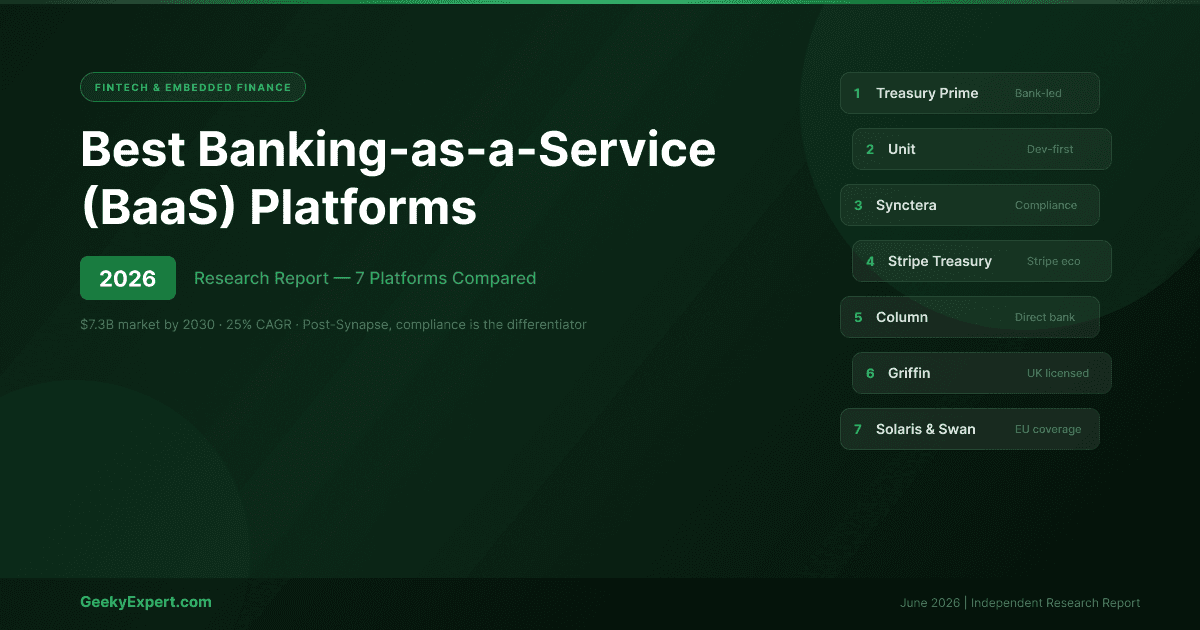

What Is Banking-as-a-Service (BaaS)? Banking-as-a-Service (BaaS) is the delivery of regulated banking capabilities -- accounts, cards, payments, lending, KYC, and compliance -- through APIs, so non-bank companies can embed financial services into their own products without becoming a licensed bank. A licensed bank sits in the background holding deposits and the charter; the BaaS provider handles orchestration and compliance tooling; and the customer-facing brand owns the user experience. The broader fintech-as-a-service market is valued at roughly $135.72 billion in 2026. Critically, the category has been reshaped by the 2023--2024 regulatory tightening and several high-profile BaaS failures, making compliance depth and bank-relationship structure the decisive selection criteria. For related research on fintech automation, see our report on the best chargeback management software . For AI-powered business tools, see our best AI agents for business automation report. ⚡ Quick Answer What is the best Banking-as-a-Service (BaaS) platform in 2026? The best BaaS platform in 2026 is Treasury Prime for fintechs that want control over bank relationships -- its multi-bank model gives you direct contracts with multiple partner banks, pricing leverage, and ~2-week go-live. Unit is the most developer-friendly all-in-one option, Synctera is the most compliance-first, and Stripe Treasury is best if you're already on Stripe. 🏆 Top Pick Overall Treasury Prime Multi-bank direct contracts, 2M+ accounts, 15+ partner banks, ~2-week go-live. Best for your situation ▸ Control over bank relationships: Treasury Prime -- multi-bank model ▸ Developer-first all-in-one: Unit -- simplest API & pricing ▸ Compliance-first: Synctera -- community banks, deep BSA tooling ▸ Already on Stripe: Stripe Treasury -- no new infrastructure VERIFIED PLATFORM DATA (2026) Platform Model Region Key Detail Treasury Prime Multi-bank, direct contracts US 2M+ accounts, 15+ banks, $103M funding, ~2-wk go-live Unit All-in-one, single-vendor US Founded 2019, NY; developer-friendly, simpler pricing Synctera Community-bank matching US Founded 2020; $94M raised; compliance-first Stripe Treasury Stripe-ecosystem US Partners Goldman Sachs, Evolve Bank Column Chartered bank (own license) US Direct bank access, no BaaS middleman Griffin Fully licensed (PRA/FCA) UK Holds funds at Bank of England Solaris / Swan Licensed BaaS EU Accounts, cards, lending (Solaris); SEPA (Swan) Why Compliance Structure Now Decides BaaS Choice (2026) The 2023--2024 BaaS shakeout changed the rules. Before, speed-to-launch was the selling point and seed-stage startups onboarded easily. After, regulators tightened oversight, several middleware BaaS providers failed, and banks narrowed risk appetite. Now in 2026, providers raised the bar -- many accept mainly Series C+ or public-company fintechs. Compliance, reconciliation, and BSA tooling are now core product, not afterthoughts. "Direct" bank-contract models (Treasury Prime, Column) reduce the tri-party risk that caused several high-profile collapses. How BaaS Models Differ (and Why It Matters) THREE BaaS STRUCTURES (2026) Model Providers How It Works Trade-off Multi-Bank / Direct Contract Treasury Prime You hold direct contracts with multiple banks; pricing leverage; swap or add banks; less lock-in You own more of the compliance program Single-Vendor / All-in-One Unit, Synctera, Stripe Treasury One platform orchestrates the bank relationship; simpler to start; turn-key compliance tooling More dependence on the provider Own-License / Chartered Column (US), Griffin (UK) The provider IS the bank -- no middleman layer; removes tri-party risk entirely Less flexibility than multi-bank